Depreciable assets are disposed of by retiring, selling, or exchanging them. When a depreciable asset is disposed of, an entry is made to recognize any unrecorded depreciation expense up to the date of the disposition, and then the asset's cost and accumulated depreciation are removed from the respective general ledger accounts. Any recognized losses or gains associated with the disposition are recorded in a separate account and appear in the portion of the income statement named other income/(expense), net.

Music World Partial Income Statement For the Year Ended June 30, 20X3

|

Operating Income

|

|

|

|

Other lncome/(Expense), Net

|

|

245,500

|

|

Interest Income

|

$ 7,500

|

|

|

Gain on Sale of Equipment

|

1,500

|

|

|

Interest Expense

|

(18,000)

|

|

|

Other lncome/(Expense), Net

|

|

(9,000)

|

|

Net Income

|

|

$236,500

|

Retirement of depreciable assets. Retirement occurs when a depreciable asset is taken out of service and no salvage value is received for the asset. In addition to removing the asset's cost and accumulated depreciation from the books, the asset's net book value, if it has any, is written off as a loss.

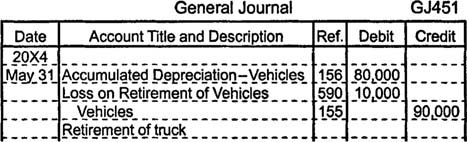

Suppose the $90,000 truck reaches the end of its useful life with a net book value of $10,000, but the truck is in such poor condition that a salvage yard simply agrees to haul it away for free. The entry to record the truck's retirement debits accumulated depreciation‐vehicles for $80,000, debits loss on retirement of vehicles for $10,000, and credits vehicles for $90,000. The loss is considered an expense and decreases net income.

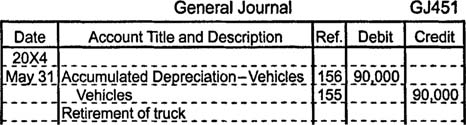

A gain never occurs when an asset is retired. If the entire cost of an asset has been depreciated before it is retired, however, there is no loss. For example, if the company using the truck had expected no salvage value and, therefore, had allocated $90,000 in depreciation expense to the truck before its retirement, the disposition would be recorded simply by debiting accumulated depreciation‐vehicles for $90,000 and crediting vehicles for $90,000.

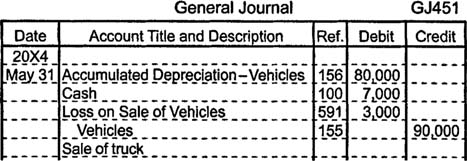

Sale of depreciable assets. If an asset is sold for cash, the amount of cash received is compared to the asset's net book value to determine whether a gain or loss has occurred. Suppose the truck sells for $7,000 when its net book value is $10,000, resulting in a loss of $3,000. The sale is recorded by debiting accumulated depreciation‐vehicles for $80,000, debiting cash for $7,000, debiting loss on sale of vehicles for $3,000, and crediting vehicles for $90,000.

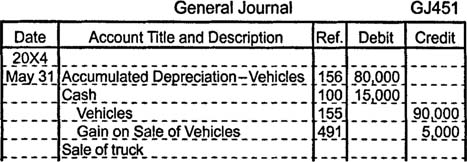

If the truck sells for $15,000 when its net book value is $10,000, a gain of $5,000 occurs. The sale is recorded by debiting accumulated depreciation‐vehicles for $80,000, debiting cash for $15,000, crediting vehicles for $90,000, and crediting gain on sale of vehicles for $5,000.

Exchange of depreciable assets. Certain types of assets, particularly vehicles and large pieces of equipment, are frequently exchanged for other tangible assets. For example, an old vehicle and a negotiated amount of cash may be exchanged for a new vehicle.

There are two types of exchanges: similar exchanges and dissimilar exchanges. A similar exchange involves the exchange of one asset for another asset that performs the same type of function. Trading in an old delivery truck to purchase a new delivery truck is an example of a similar exchange. A dissimilar exchange, which is less common than a similar exchange, involves the exchange of one asset for another asset that performs a different function. Trading in an old truck for a forklift is an example of a dissimilar exchange.

Suppose a $90,000 delivery truck with a net book value of $10,000 is exchanged for a new delivery truck. The company receives a $6,000 trade‐in allowance on the old truck and pays an additional $95,000 for the new truck, so a loss on exchange of $4,000 must be recognized.

|

Cost of Truck Traded In

|

$90,000

|

|

Less: Accumulated Depreciation

|

(80,000)

|

|

Net Book Value

|

10,000

|

|

Trade-in Value

|

(6,000)

|

|

Loss on Exchange

|

$4,000

|

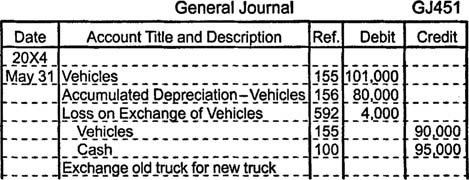

The cost of the new truck is $101,000 ($95,000 cash + $6,000 trade‐in allowance). Therefore, the exchange is recorded by debiting vehicles for $101,000 (to record the new truck's cost), debiting accumulated depreciation‐vehicles for $80,000 (to remove the old truck's accumulated depreciation from the books), debiting loss on exchange of vehicles for $4,000, crediting vehicles for $90,000 (to remove the old truck from the books), and crediting cash for $95,000.

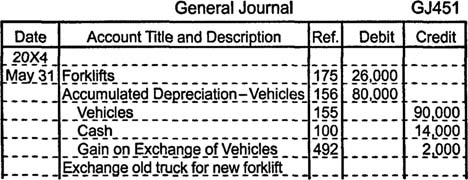

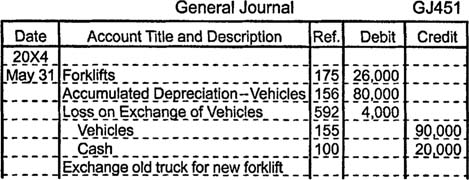

If the company exchanges its used truck for a forklift, receives a $6,000 trade‐in allowance, and pays $20,000 for the forklift, the loss on exchange is still $4,000. Assuming the company uses a separate account to record the cost of forklifts, the journal entry to record this dissimilar exchange debits forklifts for $26,000, debits accumulated depreciation‐vehicles for $80,000, debits loss on exchange of vehicles for $4,000, credits vehicles for $90,000, and credits cash for $20,000.

If the company receives a $12,000 trade‐in allowance, a gain of $2,000 occurs.

|

Cost of Truck Traded In

|

$90,000

|

|

Less: Accumulated Depreciation

|

(80,000)

|

|

Net Book Value

|

10,000

|

|

Trade-in Value

|

(12,000)

|

|

Gain on Exchange

|

($ 2,000)

|

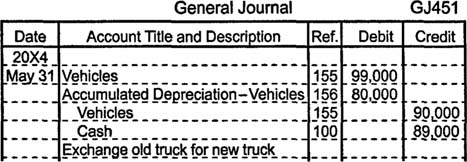

Gains on similar exchanges are handled differently from gains on dissimilar exchanges. On a similar exchange, gains are deferred and reduce the cost of the new asset. For example, after receiving a $12,000 trade‐in allowance on a delivery truck with a net book value of $10,000 and paying $89,000 in cash for a new delivery truck, the company records the cost of the new truck at $99,000 instead of $101,000. The $99,000 cost of the new truck equals the $12,000 trade‐in allowance plus the $89,000 cash payment minus the $2,000 gain. Since the $12,000 trade‐in allowance minus the $2,000 gain equals the old truck's net book value of $10,000, however, it is easier to think of the $99,000 cost as being equal to the old truck's net book value of $10,000 plus the $89,000 paid in cash. To record this exchange, the company debits vehicles for $99,000 (to record the new truck's recognized cost), debits accumulated depreciation‐vehicles for $80,000 (to remove the old truck's accumulated depreciation from the books), credits vehicles for $90,000 (to remove the old truck from the books), and credits cash for $89,000.

Gains on dissimilar exchanges are recognized when the transaction occurs. After receiving a $12,000 trade‐in allowance on a truck with a $10,000 net book value and paying $14,000 in cash for a forklift, the company debits forklifts for $26,000, debits accumulated depreciation‐vehicles for $80,000, credits vehicles for $90,000, credits cash for $14,000, and credits gain on exchange of vehicles for $2,000.