Recording Notes Receivable Transactions

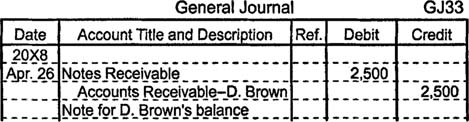

Customers frequently sign promissory notes to settle overdue accounts receivable balances. For example, if a customer named D. Brown signs a six‐month, 10%, $2,500 promissory note after falling 90 days past due on her account, the business records the event by debiting notes receivable for $2,500 and crediting accounts receivable from D. Brown for $2,500. Notice that the entry does not include interest revenue, which is not recorded until it is earned.

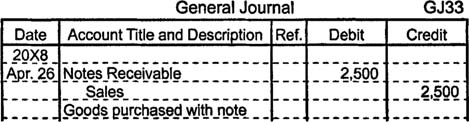

If a customer signs a promissory note in exchange for merchandise, the entry is recorded by debiting notes receivable and crediting sales.

A company that frequently exchanges goods or services for notes would probably include a debit column for notes receivable in the sales journal so that such transactions would not need to be recorded in the general journal. A separate subsidiary ledger for notes receivable may also be created. If the amount of notes receivable is significant, a company should establish a separate allowance for bad debts account for notes receivable.

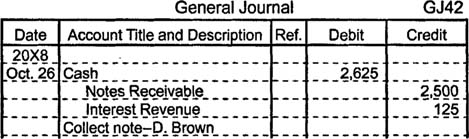

When a note's maker pays according to the terms specified on the note, the note is said to be honored. Assuming that no adjusting entries have been made to accrue interest revenue, the honored note is recorded by debiting cash for the amount the customer pays, crediting notes receivable for the principal value of the note, and crediting interest revenue for the interest earned. The total interest on a six‐month, 10%, $2,500 note is $125, so if D. Brown honors her note, the entry includes a $2,625 debit to cash, a $2,500 credit to notes receivable, and a $125 credit to interest revenue.

If some of the interest has already been accrued (through adjusting entries that debited interest receivable and credited interest revenue), then the previously accrued interest is credited to interest receivable and the remainder of the interest is credited to interest revenue.

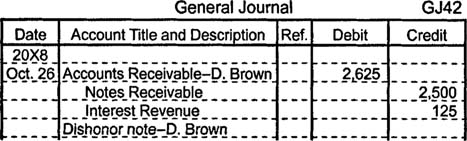

When the maker of a promissory note fails to pay, the note is said to be dishonored. The dishonored note may be recorded in one of two ways, depending upon whether or not the payee expects to collect the debt If payment is expected, the company transfers the principal and interest to accounts receivable, removes the face value of the note from notes receivable, and recognizes the interest revenue. Assuming D. Brown dishonors the note but payment is expected, the company records the event by debiting accounts receivable from D. Brown for $2,625, crediting notes receivable for $2,500, and crediting interest revenue for $125.

If D. Brown dishonors the note and the company believes the note is a bad debt, allowance for bad debts is debited for $2,500 and notes receivable is credited for $2,500. No interest revenue is recognized because none will ever be received.

If interest on a bad debt had previously been accrued, then a correcting entry is needed to remove the accrued interest from interest revenue and interest receivable (by debiting interest revenue and crediting interest receivable). Although interest revenue would have been overstated in the accounting periods when the interest was accrued and would be understated in the period when the correcting entry occurs, efforts to amend prior statements or recognize the error in footnotes on forthcoming statements are not necessary except in rare situations where the bad debt changes reported revenue so much that the judgment of those who use financial statements is materially affected by the disclosure.