The Cottage Gang is considering the purchase of $150,000 of equipment for its boat rentals. The equipment is expected to last seven years and have a $5,000 salvage value at the end of its life. The annual cash inflows are expected to be $250,000 and the annual cash outflows are estimated to be $200,000.

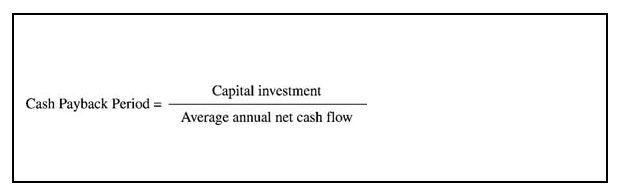

The payback measures the length of time it takes a company to recover in cash its initial investment. This concept can also be explained as the length of time it takes the project to generate cash equal to the investment and pay the company back. It is calculated by dividing the capital investment by the net annual cash flow. If the net annual cash flow is not expected to be the same, the average of the net annual cash flows may be used.

![]()

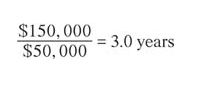

For the Cottage Gang, the cash payback period is three years. It was calculated by dividing the $150,000 capital investment by the $50,000 net annual cash flow ($250,000 inflows ‐ $200,000 outflows) ![]()

The shorter the payback period, the sooner the company recovers its cash investment. Whether a cash payback period is good or poor depends on the company's criteria for evaluating projects. Some companies have specific guidelines for number of years, such as two years, while others simply require the payback period to be less than the asset's useful life.

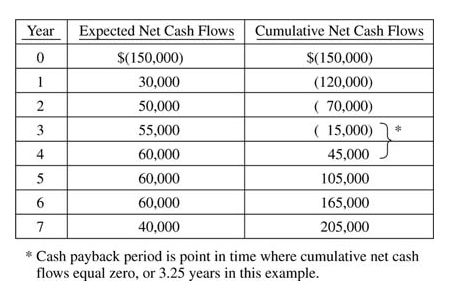

When net annual cash flows are different, the cumulative net annual cash flows are used to determine the payback period. If the Turtles Co. has a project with a cost of $150,000, and net annual cash inflows for the first seven years of the project are: $30,000 in year one, $50,000 in year two, $55,000 in year three, $60,000 in year four, $60,000 in year five, $60,000 in year six, and $40,000 in year seven, then its cash payback period would be 3.25 years. See the example that follows. ![]()

The cash payback period is easy to calculate but is actually not the only criteria for choosing capital projects. This method ignores differences in the timing of cash flows during the project and differences in the length of the project. The cash flows of two projects may be the same in total but the timing of the cash flows could be very different. For example, assume project LJM had cash flows of $3,000, $4,000, $7,000, $1,500, and $1,500 and project MEM had cash flows of $6,000, $5,000, $3,000, $2,000, and $1,000. Both projects cost $14,000 and have a payback of 3.0 years, but the cash flows are very different. Similarly, two projects may have the same payback period while one project lasts five years beyond the payback period and the second one lasts only one year.

Considering the time value of money is important when evaluating projects with different costs, different cash flows, and different service lives. Discounted cash flow techniques, such as the net present value method, consider the timing and amount of cash flows. To use the net present value method, you will need to know the cash inflows, the cash outflows, and the company's required rate of return on its investments. The required rate of return becomes the discount rate used in the net present value calculation. For the following examples, it is assumed that cash flows are received at the end of the period.

Using data for the Cottage Gang and assuming a required rate of return of 12%, the net present value is $80,452. It is calculated by discounting the annual net cash flows and salvage value using the 12% discount factors. The Cottage Gang has equal net cash flows of $50,000 ($250,000 cash receipt minus $200,000 operating costs) so the present value of the net cash flows is computed by using the present value of an annuity of 1 for seven periods. Using a 12% discount rate, the factor is 4.5638 and the present value of the net cash flows is $228,190. The salvage value is received only once, at the end of the seven years (the asset's life), so its present value of $2,262 is computed using the Present Value of 1 table factor for seven periods and 12% discount rate factor of .4523 times the $5,000 salvage value. The investment of $150,000 does not need to be discounted because it is already in today's dollars (a factor value of 1.0000). To calculate the net present value (NPV), the investment is subtracted from the present value of the total cash inflows of $230,452. See the examples that follow. Because the net present value (NPV) is positive, the required rate of return has been met.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|