In order to understand the $1,175 unfavorable monthly variance, it must be analyzed by its component parts: direct materials variances, direct labor variances, and overhead variances. Each of these variances can further be broken down into a price (rate) variance and a quantity (usage or efficiency) variance. A general template that can be used for direct materials variances, direct labor variances, and variable overhead variances uses three amounts — actual, flexible budget, and standard — as a basis for calculating the variances. ![]()

The price variance is favorable if actual costs are less than flexible budget costs. The quantity variance is favorable if flexible budget costs are less than standard costs. The total variance is favorable if the actual costs are less than standard costs.

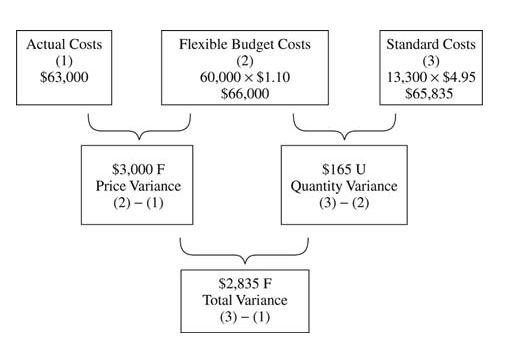

The total direct materials variance is $2,835 favorable and consists of a $3,000 favorable price variance and a $165 unfavorable quantity variance. ![]()

Actual costs of $63,000 are less than flexible budget costs of $66,000, so the materials price variance is $3,000 favorable. The variance can also be thought of on a price per unit basis. The actual costs of $63,000 were for 60,000 feet of direct material, so the actual price per foot is $1.05 ($63,000 ÷ 60,000). The original budget was for a direct materials cost of $1.10 per foot, so it was expected that 60,000 feet of material would cost $66,000. The direct materials actually cost less than budget by $0.05 per foot ($1.10 budget versus $1.05 actual), so the variance is favorable. The direct materials quantity variance of $165 unfavorable means this company used more direct materials than planned because flexible budget costs of $66,000 are higher than the standard costs of $65,825. To produce 13,300 sets of bases, the company expected a cost of $4.95 per set (4.5 feet of material at $1.10 per foot), for a total cost of $65,835. This can also be analyzed by identifying the total feet of material it should have taken to produce 13,300 sets of bases and multiplying by the cost per foot of material (13,300 sets × 4.5 feet per unit = 59,850 feet of direct materials × $1.10 per foot = $65,835). It actually used 60,000 feet, which prices out at an expected $1.10 per foot to be $66,000. The total direct materials variance is calculated by adding the price and quantity variances together or by comparing actual cost of direct materials with the standard cost of producing 13,300 sets of bases.

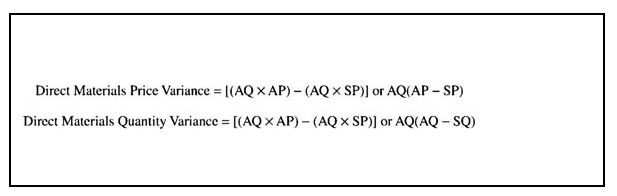

Another way of computing the direct materials variance is using formulas.

![]()

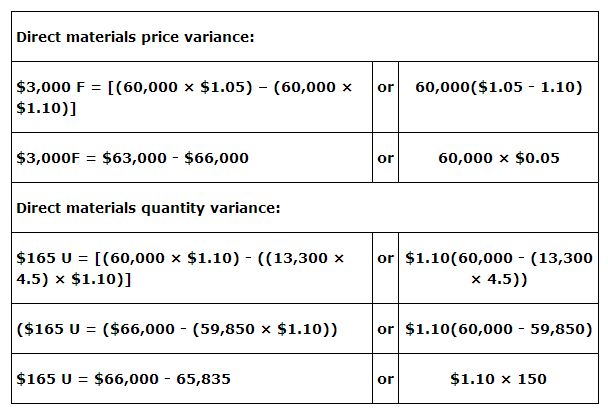

Using the formulas to calculate the variances would work like this:

Once the variances are calculated, management completes the analysis by obtaining explanations for why the variances occurred. For example, a question raised is “Why did materials cost less than planned?” As an answer, management may learn there was a price decrease, or the direct materials were acquired from another source, or lower quality materials were obtained. The explanations for price variances must relate to the cost of the direct materials, not the quantity of the materials used. Similarly, the reasons for the quantity variance need to relate to the amount of materials used, not the price paid for the materials. Reasons for a quantity variance could be more waste or scrap than was planned, or that lower quality materials were used, or less skilled workers were hired or used on the production line, or machine problems occurred that damaged materials.

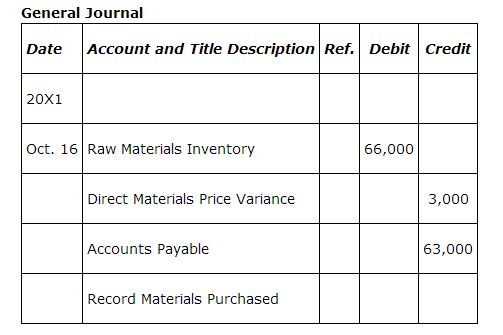

Recording direct materials variances. The direct materials price variance is recorded when the direct materials are purchased. The materials are recorded using actual quantity and standard cost. A separate account is used to track each variance.

|

|

|

|

|

|

|

|

|

|