Some companies have homogeneous or very similar products that are not made to order and are produced in large volumes. They continually process their product, moving it from one function to the next until it is completed. In these companies, the manufacturing costs incurred are allocated to the proper functions or departments within the factory process rather than to specific products. Examples of products that companies produce continuously are cereal, bread, candy, steel, automotive parts, chips, and computers. Companies that refine oil or bottle drinks and companies that provide services such as mail sorting and catalog order are also examples of continuous, homogeneous processing.

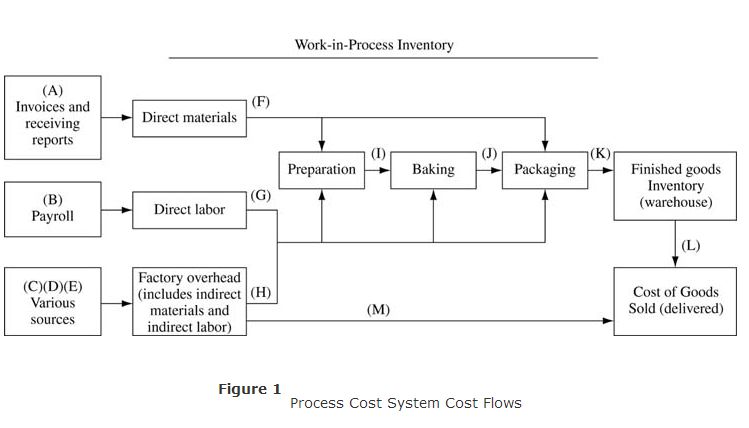

To illustrate, assume the Best Chips company manufactures potato chips. The company has three work areas they call preparation, baking, and packaging. The preparation area includes cutting potatoes and adding flavorings. Conveyor belts are used to move the product from one function to the next. In this company, raw materials are added in two of the functions: the preparation function and the packaging function. Labor and overhead are incurred in each function. Figure shows the process flow and costs associated with Best Chip's process cost system.

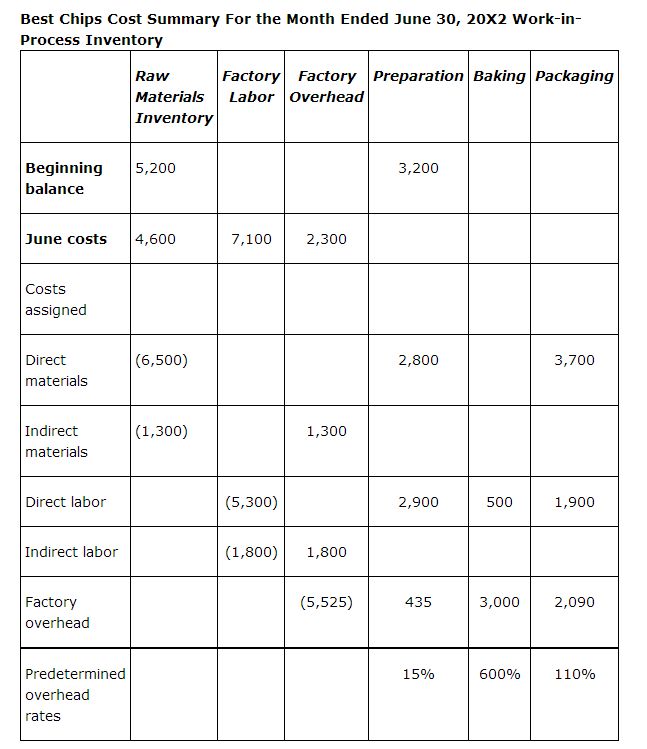

The cost report for Best Chips summarizes how manufacturing costs (direct materials, direct labor, and manufacturing overhead) are assigned to the three departments. The report for June is as follows:

The raw materials are assigned based on material requisition forms, the labor based on time tickets, and the overhead based on predetermined overhead rates based on direct labor dollars. The journal entries to record these transactions are made prior to the period end entries that transfer the amounts from one work‐in‐process inventory account to another, from work‐in‐process inventory to finished goods inventory, and from finished goods inventory to cost of goods sold. The letters of the journal entries used to illustrate the accounting for process cost systems correspond to the letters in Figure .

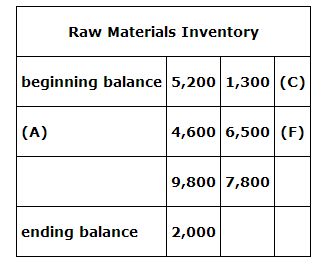

Best Chips started the month of June with $5,200 in raw materials inventory. Best Chips uses the perpetual inventory method, so raw materials purchased are added to the raw material inventory account when they are received. Raw materials requisitioned that become part of the final product or are used by a specific function are considered direct materials used. The costs of direct materials are added to the proper department's work‐in‐process inventory account. Raw materials requisitioned that are used for general production purposes are added to factory overhead. The journal entries related to raw material activity for June are:

At the end of the month, $2,000 of materials remained in raw materials inventory.

As the factory labor payroll is prepared and recorded, the payroll costs are split between those employees who work in specific functions (departments) and those involved in the general functions of the factory. The specific function costs are called direct labor and are assigned to work‐in‐process inventory. The general factory labor costs are indirect labor costs that are added to factory overhead. Unlike the accounting for payroll under the job order cost system, the employee does not have to be physically involved in making a product to be assigned to a specific function. If a specific maintenance worker or supervisor is assigned to the preparation function, their wages are allocated to that function even though these workers are not directly involved in preparing the chips to be baked. The accounting for the labor costs for June includes the following journal entries, shown in the following table.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|