|

|

|

|

|

|

![]()

Cash payments for operating expenses. This includes wages and other operating costs. To calculate the cash payments for operating expenses, two steps are required. First, the amount of total operating expenses in the income statement of $42,600 is reduced by $14,400 depreciation expense because depreciation is a non‐cash expense. Second, the balance is adjusted for changes in the balances of related balance sheet accounts. For Brothers' Quintet, Inc., the related balance sheet accounts and the changes in these account balances are: increase of $142 in prepaid expenses; increase of $320 in wages payable; and $1,295 decrease in accrued expenses. The operating expenses before depreciation expense total $28,200. To this total the increase of $142 in prepaid expenses is added, the increase of $320 in wages payable is subtracted, and the decrease of $1,295 in accrued expenses is added to get cash payments to suppliers of $29,317. As with the prior calculations, the calculation changes with the direction of the change in the balances of the related balance sheet accounts. The operating expenses excluding depreciation expense would be decreased by a decrease in the prepaid expenses account's balance, increased by a decrease in the balance of the wages payable account, and decreased by an increase in the balance of the accrued expenses account.

![]()

Cash payments for income taxes. This represents amounts paid by the company for income taxes. The amount is calculated by taking income tax expense and increasing it by the amount of any decrease in the balance of the income taxes payable account or decreasing it by the amount of any increase in the balance of the income taxes payable account. In this case, there are no accrued taxes so the income tax expense is the same as cash paid for income taxes.

![]()

Cash paid for interest. This represents amounts paid by the company for interest. The amount is calculated by taking interest expense and increasing it by the amount of any decrease in the balance of the interest payable account or decreasing it by the amount of an increase in the balance of the interest payable account. In this case, there is no balance in the accrued interest account at the end of the period so the cash paid for interest is the same as the interest expense.

![]()

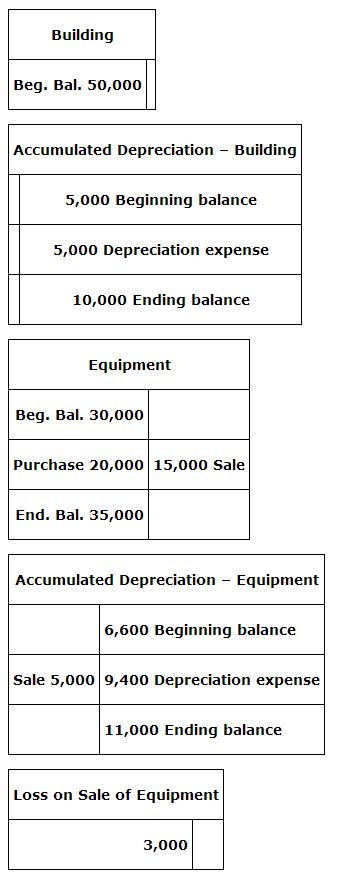

To identify the investing activities, the long‐term asset accounts must be analyzed.

Purchase of equipment This includes the amount of cash paid for equipment. If a note had been taken in exchange for a portion of or all of the purchase price of the equipment, only the cash actually paid would be reported as a payment on the statement of cash flows. The portion of the purchase price represented by the note would be separately disclosed if it were a material amount.

Proceeds from sale of equipment (or any other long‐term asset). The cash received from the sale is reported here. The proceeds are not adjusted for any gain or loss that may also have been recorded on the sale because only the proceeds represent cash, the gain or loss represents the difference between the book value of the assets and the value received. For the Brothers' Quintet, Inc., the book value is $10,000 ($15,000 cost – $5,000 accumulated depreciation). The loss is $3,000, calculated by subtracting the $10,000 book value from the proceeds of $7,000, and is reported in the income statement. The proceeds of $7,000 represent the actual cash received from the sale and is the amount reported in the statement of cash flows. The analysis of long‐term asset accounts includes the following:

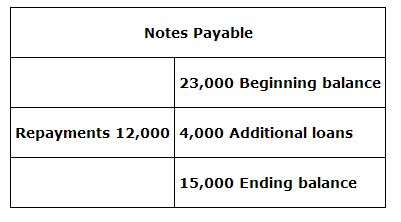

To identify the financing activities, the long‐term liability accounts and the stockholders' equity accounts must be analyzed.

Proceeds for bank loan. Proceeds for bank loan of $4,000 represents additional borrowings during the year. Borrowings are not shown net of repayments. Each is treated as a separate activity to be reported on the statement of cash flows.

Payment on loan. Payment on loan of $12,000 equals the cash repayments made to the bank during the year.

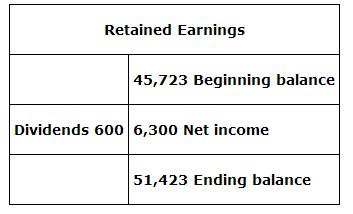

Proceeds from sale of stock. This represents the cash received from the issuance of new shares to investors.

|

|

Cash payments of dividends. This is the amount of dividends paid during the year. As the statement of cash flows includes only cash activity, the declaration of a dividend does not result in any reporting on the statement, it is only when the dividends are paid that they are included in the statement cash flows. In analyzing the retained earnings account, the other activity is the net income. The cash activities related to generating net income are included in the operating activities section of the statement of cash flows, and therefore, are not included in the financing activities section.

If the direct method of preparing the statement of cash flows is used, the Financial Accounting Standards Board requires companies to disclose the reconciliation of net income to the net cash provided by (used by) operating activities that would have been reported if the indirect method had been used to prepare the statement.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|