The job order cost system is used when products are made based on specific customer orders. Each product produced is considered a job. Costs are tracked by job. Services rendered can also be considered a job. For example, service companies consider the creation of a financial plan by a certified financial planner, or of an estate plan by an attorney, unique jobs. The job order cost system must capture and track by job the costs of producing each job, which includes materials, labor, and overhead in a manufacturing environment. To track data, the following documents are used:

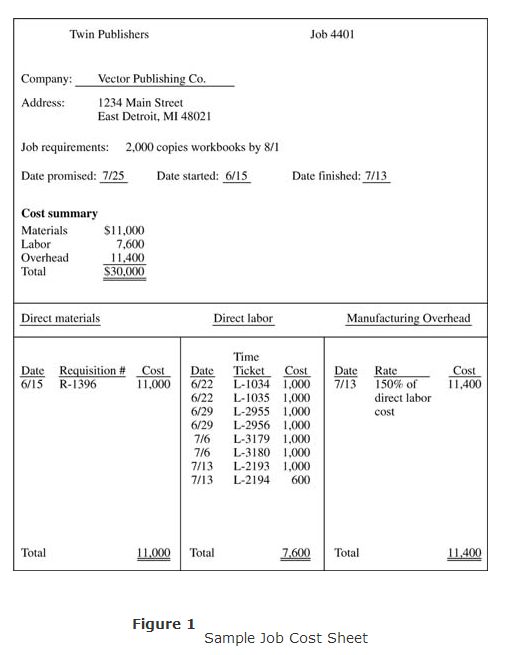

Job cost sheet. This is used to track the job number; customer information; job information (date started, completed, and shipped); individual cost information for materials used, labor, and overhead; and a total job cost summary. See Figure 1.

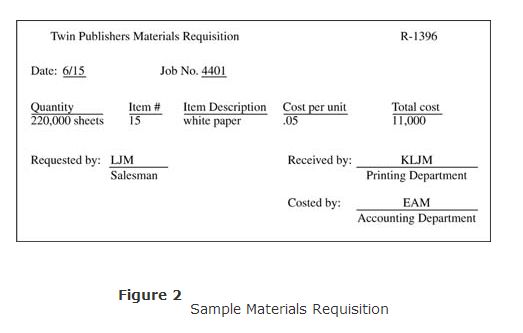

Materials requisition form. To assure that materials costs are properly allocated to jobs in process, a materials requisition form (see Figure 2) is usually completed as materials are taken from the raw materials inventory and added to work‐in‐process.

Time ticket. Labor costs are allocated to work‐in‐process inventory based on the completion of time tickets (see Figure 3) identifying what job a worker spent time on.

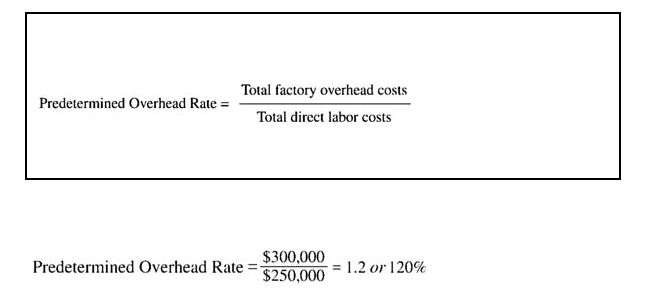

Factory overhead costs are allocated to jobs in process using a predetermined overhead rate. The predetermined overhead rate is determined by estimating (during the budget process) total factory overhead costs and dividing these total costs by direct labor hours or direct labor dollars. For example, assume a company using direct labor dollars for the allocation of overhead estimated its total overhead costs to be $300,000 and total direct labor dollars to be $250,000. The company's predetermined overhead rate for allocating overhead to jobs in process is 120% of direct labor dollars, and is calculated as follows:

![]()

![]()

If direct labor costs are $20,000 for the month, overhead of $24,000 ($20,000 × 120%) would be allocated to work‐in‐process inventory. Factory overhead would be allocated to individual jobs based on the portion of the $20,000 direct labor cost that is assigned to each job. If job number 45 had $9,000 in direct labor cost for the month, factory overhead of $10,800 ($9,000 × 120%) would also be allocated to the job.

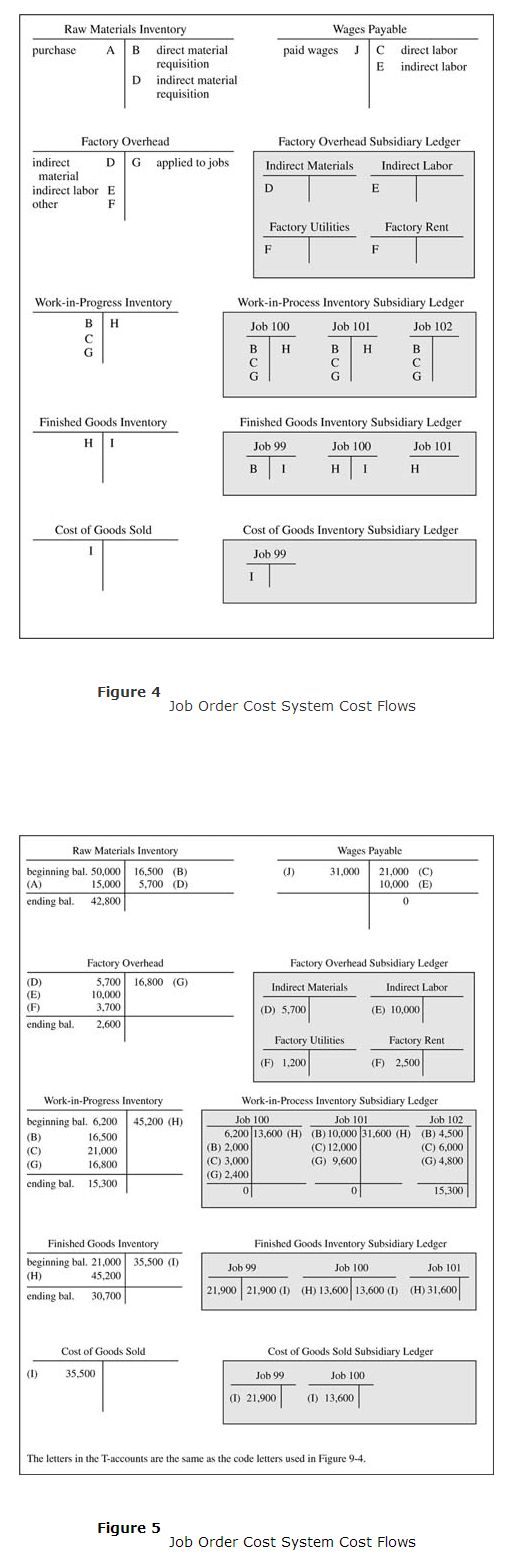

Once a job is completed, the total costs assigned to the job are transferred from work‐in‐process inventory to finished goods inventory. Once the job is sold and delivered, the job costs are transferred from finished goods inventory to cost of goods sold. Figure 4 summarizes the flow of costs in a job order cost system and Figure 5 summarizes the journal entries required given the flow of costs in Figure 4. The ending balances in the three inventory accounts would be reported as inventories on the balance sheet and cost of goods sold would be reported on the income statement.

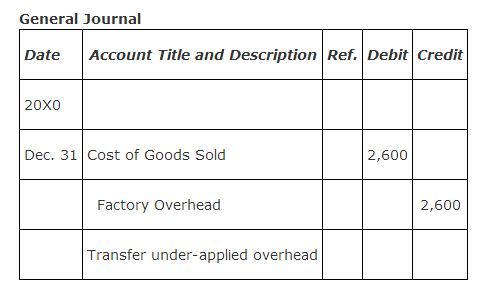

The factory overhead account (see Figure 5) has a balance which indicates the amount of overhead applied to work‐in‐process inventory is different from the actual overhead incurred. When there is a debit balance in the factory overhead account, it is called under‐applied overhead meaning not enough overhead was allocated to jobs. If the balance in the factory overhead account was a credit, the overhead would be over‐applied, meaning too much overhead was allocated to jobs. Factory overhead must be zero at the end of the year. Most companies transfer the balance in factory overhead to cost of goods sold. An alternative method, although more complex, is to allocate the under‐ or over‐applied balance among the work‐in‐process inventory, finished goods inventory, and cost of goods sold accounts. The $2,600 account balance in factory overhead in Figure 5 is relatively small. To zero out the account balance and transfer it to cost of goods sold, the entry would be:

Key:

- A Purchased raw materials

- B Direct material requisition to be used on jobs

- C Direct labor payroll based on time ticket

- D Indirect materials used

- E Indirect labor payroll

- F Other overhead costs incurred

- G Overhead applied to jobs (direct labor dollars ¥ 80% predetermined overhead rate)

- H Transfer completed jobs to finished goods inventory

- I Transferred sold jobs to cost of goods sold

- J Paid wages

The journal entries that follow support the transactions in Figure 5.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|