Labor Demand and Supply in a Perfectly Competitive Market

In addition to making output and pricing decisions, firms must also determine how much of each input to demand. Firms may choose to demand many different kinds of inputs. The two most common are labor and capital.

The demand and supply of labor are determined in the labor market. The participants in the labor market are workers and firms. Workers supply labor to firms in exchange for wages. Firms demand labor from workers in exchange for wages.

The firm's demand for labor. The firm's demand for labor is a derived demand; it is derived from the demand for the firm's output. If demand for the firm's output increases, the firm will demand more labor and will hire more workers. If demand for the firm's output falls, the firm will demand less labor and will reduce its work force.

Marginal revenue product of labor. When the firm knows the level of demand for its output, it determines how much labor to demand by looking at the marginal revenue product of labor. The marginal revenue product of labor (or any input) is the additional revenue the firm earns by employing one more unit of labor. The marginal revenue product of labor is related to the marginal product of labor. In a perfectly competitive market, the firm's marginal revenue product of labor is the value of the marginal product of labor.

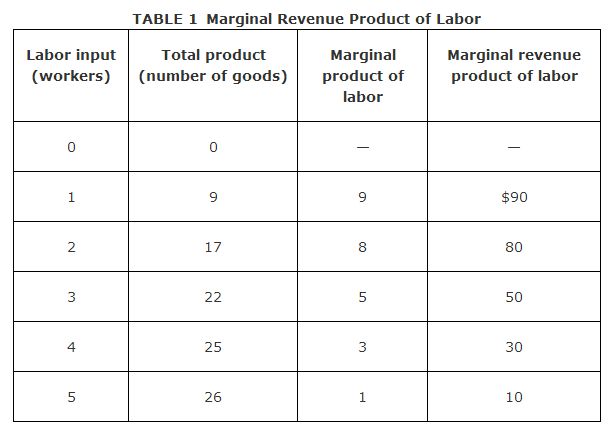

For example, consider a perfectly competitive firm that uses labor as an input. The firm faces a market price of $10 for each unit of its output. The total product, marginal product, and marginal revenue product that the firm receives from hiring 1 to 5 workers are reported in Table .

The marginal revenue product of each additional worker is found by multiplying the marginal product of each additional worker by the market price of $10. The marginal revenue product of labor is the additional revenue that the firm earns from hiring an additional worker; it represents the wage that the firm is willing to pay for each additional worker. The wage that the firm actually pays is the market wage rate, which is determined by the market demand and market supply of labor. In a perfectly competitive labor market, the individual firm is a wage‐taker; it takes the market wage rate as given, just as the firm in a perfectly competitive product market takes the price for its output as given. The market wage rate in a perfectly competitive labor market represents the firm's marginal cost of labor, the amount the firm must pay for each additional worker that it hires.

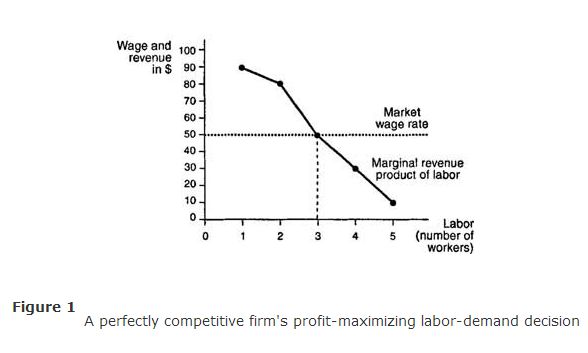

The perfectly competitive firm's profit‐maximizing labor‐demand decision is to hire workers up to the point where the marginal revenue product of the last worker hired is just equal to the market wage rate, which is the marginal cost of this last worker. For example, if the market wage rate is $50 per worker per day, the firm—whose marginal revenue product of labor is given in Table —would choose to hire 3 workers each day.

The firm's labor demand curve. The firm's profit‐maximizing labor‐demand decision is depicted graphically in Figure .

This figure graphs the marginal revenue product of labor data from Table along with the market wage rate of $50. When the marginal revenue product of labor is graphed, it represents the firm's labor demand curve. The demand curve is downward sloping due to the law of diminishing returns; as more workers are hired, the marginal product of labor begins declining, causing the marginal revenue product of labor to fall as well. The intersection of the marginal revenue product curve with the market wage determines the number of workers that the firm hires, in this case 3 workers.

An individual's supply of labor. An individual's supply of labor depends on his or her preferences for two types of “goods”: consumption goods and leisure. Consumption goods include all the goods that can be purchased with the income that an individual earns from working. Leisure is the good that individuals consume when they are not working. By working more (supplying more labor), an individual reduces his or her consumption of leisure but is able to increase his or her purchases of consumption goods.

In choosing between leisure and consumption, the individual faces two constraints. First, the individual is limited to twenty‐four hours per day for work or leisure. Second, the individual's income from work is limited by the market wage rate that the individual receives for his or her labor skills. In a perfectly competitive labor market, workers—like firms—are wage‐takers; they take the market wage rate that they receive as given.

An individual's labor supply curve. An example of an individual's labor supply curve is given in Figure .

As wages increase, so does the opportunity cost of leisure. As leisure becomes more costly, workers tend to substitute more work hours for fewer leisure hours in order to consume the relatively cheaper consumption goods, which is the substitution effect of a higher wage.

An income effect is also associated with a higher wage. A higher wage leads to higher real incomes, provided that prices of consumption goods remain constant. As real incomes rise, individuals will demand more leisure, which is considered a normal good—the higher an individual's income, the easier it is for that individual to take more time off from work and still maintain a high standard of living in terms of consumption goods.

The substitution effect of higher wages tends to dominate the income effect at low wage levels, while the income effect of higher wages tends to dominate the substitution effect at high wage levels. The dominance of the income effect over the substitution effect at high wage levels is what accounts for the backward‐bending shape of the individual's labor supply curve.

Market demand and supply of labor. Many different markets for labor exist, one for every type and skill level of labor. For example, the labor market for entry level accountants is different from the labor market for tennis pros. The demand for labor in a particular market—called the market demand for labor—is the amount of labor that all the firms participating in that market will demand at different market wage levels. The market demand curve for a particular type of labor is the horizontal summation of the marginal revenue product of labor curves of every firm in the market for that type of labor. The market supply of labor is the number of workers of a particular type and skill level who are willing to supply their labor to firms at different wage levels. The market supply curve for a particular type of labor is the horizontal summation of the individuals' labor supply curves. Unlike an individual's supply curve, the market supply curve is not backward bending because there will always be some workers in the market who will be willing to supply more labor and take less leisure time, even at relatively high wage levels.

![]()

![]()